When planning for retirement, choosing the right savings vehicle can significantly impact your financial future. Among the most popular options, Roth IRA and 401(k) accounts stand out as powerful tools to help secure your golden years. However, understanding their differences, benefits, and limitations is essential to making an informed decision.

Both a Roth IRA and a 401(k) offer unique advantages, but they cater to different financial needs and goals. While a 401(k) is typically employer-sponsored and offers pre-tax contributions, a Roth IRA allows for after-tax contributions with tax-free withdrawals during retirement. Selecting between the two—or even combining them—requires careful consideration of your income, tax bracket, and long-term objectives.

If you're unsure about the best choice for your retirement planning, this comprehensive guide will provide a detailed comparison of Roth IRA vs 401(k). From tax implications to contribution limits and withdrawal rules, we'll cover the key aspects to help you make a confident decision. Let's dive into the nuances of these two retirement savings options and explore which one aligns with your financial aspirations.

Table of Contents

- What is a Roth IRA?

- What is a 401(k)?

- How does a Roth IRA differ from a 401(k)?

- What are the tax benefits of Roth IRA vs 401(k)?

- How do contribution limits compare?

- Can you have both a Roth IRA and a 401(k)?

- Who should choose a Roth IRA over a 401(k)?

- Which is better for tax-free income?

- Withdrawal rules and penalties

- Are there income limits to consider?

- Can my employer match my contributions?

- What are the fees associated with each?

- How to decide between a Roth IRA and a 401(k)?

- Common mistakes to avoid

- Final thoughts on Roth IRA vs 401(k)

What is a Roth IRA?

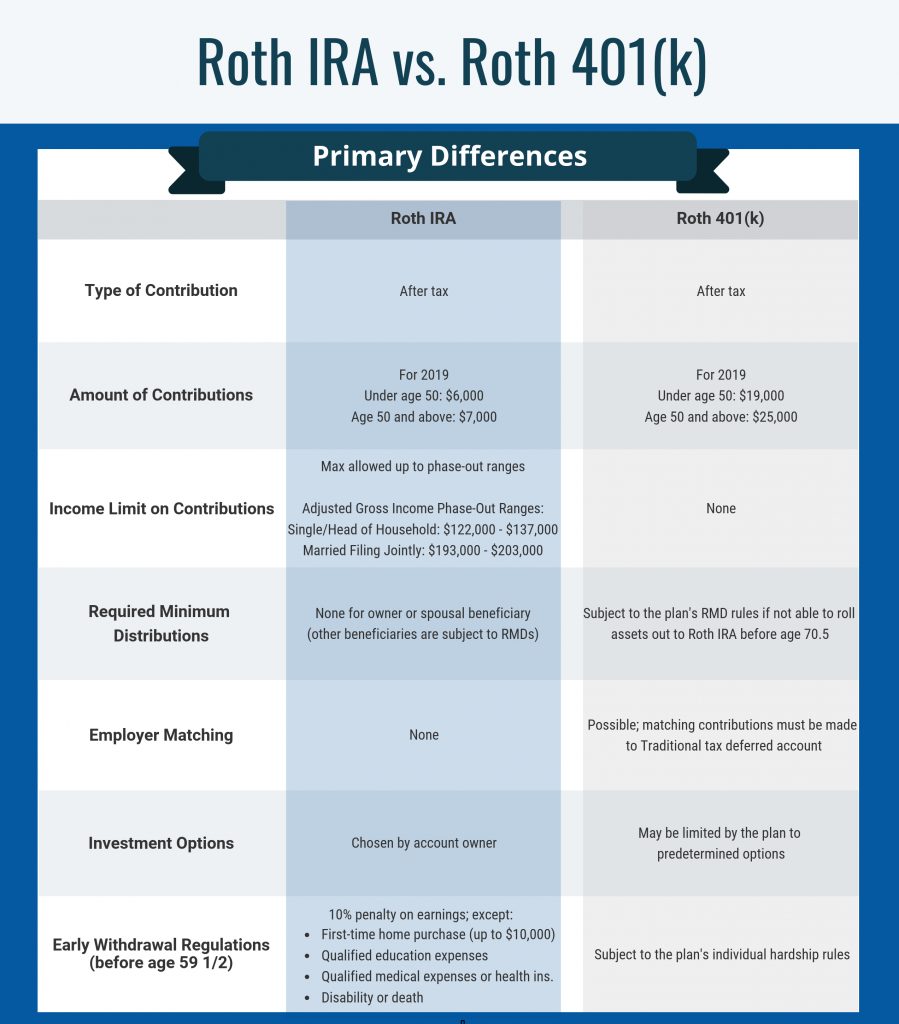

A Roth IRA (Individual Retirement Account) is a retirement savings account that allows individuals to contribute after-tax income. The primary benefit of a Roth IRA is that withdrawals during retirement are tax-free, including both contributions and earnings, provided specific conditions are met. This makes it an excellent option for those who expect to be in a higher tax bracket in retirement.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement plan where employees can contribute pre-tax income, reducing their taxable income for the year. Employers often match a portion of employee contributions, providing additional savings. The earnings in a 401(k) grow tax-deferred, and taxes are paid upon withdrawal during retirement.

How does a Roth IRA differ from a 401(k)?

While both Roth IRAs and 401(k)s are designed to help individuals save for retirement, they differ in several key ways:

- Tax Treatment: Roth IRAs use after-tax contributions, while 401(k)s use pre-tax contributions.

- Contribution Limits: 401(k)s generally allow higher contribution limits compared to Roth IRAs.

- Employer Match: 401(k) plans often include employer-matching contributions; Roth IRAs do not.

- Income Limits: Roth IRAs have income eligibility limits, whereas 401(k)s do not.

What are the tax benefits of Roth IRA vs 401(k)?

The tax treatment of Roth IRAs and 401(k)s is one of their most significant differences. Roth IRAs offer tax-free withdrawals during retirement, while 401(k)s provide tax-deferred growth and reduce taxable income in the year of contribution. Understanding your current and future tax situation is crucial to determining which option offers the greatest benefit.

How do contribution limits compare?

Contribution limits for Roth IRAs and 401(k)s differ significantly:

- Roth IRA: As of 2023, individuals can contribute up to $6,500 annually, or $7,500 if aged 50 or older.

- 401(k): Employees can contribute up to $22,500 annually, or $30,000 if aged 50 or older, in 2023.

Can you have both a Roth IRA and a 401(k)?

Yes, you can contribute to both a Roth IRA and a 401(k) simultaneously, provided you meet the income eligibility requirements for the Roth IRA. This strategy allows you to benefit from the unique advantages of both accounts, offering a diversified approach to retirement savings.

Who should choose a Roth IRA over a 401(k)?

A Roth IRA might be the better choice for individuals who:

- Expect to be in a higher tax bracket during retirement.

- Want more control over their investment options.

- Do not have access to an employer-sponsored 401(k) plan.

Which is better for tax-free income?

For those prioritizing tax-free income during retirement, a Roth IRA is the superior option. Contributions are made with after-tax dollars, and qualified withdrawals in retirement are entirely tax-free. In contrast, 401(k) withdrawals are taxed as ordinary income.

Withdrawal rules and penalties

Understanding the withdrawal rules for Roth IRAs and 401(k)s is essential:

- Roth IRA: Contributions can be withdrawn at any time without penalty. Earnings are tax-free if the account has been open for at least five years and the account holder is aged 59½ or older.

- 401(k): Withdrawals before 59½ incur a 10% penalty and are subject to income tax unless an exception applies.

Are there income limits to consider?

Roth IRAs have income eligibility limits based on modified adjusted gross income (MAGI). For 2023, contributions begin to phase out at $138,000 for single filers and $218,000 for married couples filing jointly. In contrast, 401(k) plans do not have income limits for contributions.

Can my employer match my contributions?

Employer matching is a significant advantage of 401(k) plans. Many employers match a percentage of employee contributions, effectively providing free money for retirement savings. Roth IRAs, being individual accounts, do not offer employer matching.

What are the fees associated with each?

Fees vary between Roth IRAs and 401(k)s, depending on the provider and investment options:

- Roth IRA: Typically, fees are associated with the investments chosen within the account, such as mutual fund expense ratios.

- 401(k): Fees may include administrative costs, investment management fees, and other plan-related expenses.

How to decide between a Roth IRA and a 401(k)?

When choosing between a Roth IRA and a 401(k), consider these factors:

- Your current and expected future tax brackets.

- Whether your employer offers a 401(k) with matching contributions.

- Your income level and eligibility for a Roth IRA.

- Your preference for investment options and flexibility.

Common mistakes to avoid

When planning for retirement, avoid these common mistakes:

- Not contributing enough to receive the full employer match in your 401(k).

- Overlooking the tax benefits of a Roth IRA.

- Failing to diversify retirement savings across multiple accounts.

- Ignoring plan fees and their impact on long-term growth.

Final thoughts on Roth IRA vs 401(k)

Deciding between a Roth IRA and a 401(k) depends on your unique financial situation, goals, and preferences. Both accounts offer valuable benefits, and in many cases, combining them can provide the best of both worlds. By understanding their differences and aligning them with your retirement strategy, you can build a secure financial future.

You Might Also Like

How Much Are Super Bowl Tickets? A Complete Guide To Costs And InsightsUnique And Thoughtful Ideas For A 5 Year Anniversary Gift

Understanding The Profound Meaning Of "Allahu Akbar"

Unlocking The Meaning And Significance Of The 818 Angel Number

The Ultimate Guide To Sous Vide Machines: Revolutionizing Home Cooking

Article Recommendations

- The Dynamic Duo Hannah Vanorman And Jonathan Roumie

- Clarkgable_0.xml

- Unveiling The Mystery Of Tom Burke Wife Everything You Need To Know