The average mortgage rate is a critical metric for homeowners, prospective buyers, and investors alike. It serves as a barometer for understanding current borrowing costs and the overall state of the housing market. Whether you're planning to purchase your first home, refinance an existing loan, or simply stay informed about economic trends, knowing the average mortgage rate is essential. This rate not only impacts your monthly mortgage payments but also provides insight into broader economic conditions, such as inflation and monetary policy.

In today’s fast-paced real estate market, the fluctuations in the average mortgage rate can make a significant difference in affordability. A small change in the rate can translate into hundreds or even thousands of dollars over the life of a loan. That’s why staying updated on these changes is vital, especially for those in the process of making major financial decisions. With interest rates often fluctuating due to economic factors, this guide will provide you with everything you need to know.

This article delves into the dynamics of the average mortgage rate, breaking down its components, trends, and implications. From understanding how rates are calculated to exploring factors that influence them, we’ll cover it all. Additionally, we’ll answer common questions, provide actionable tips for securing the best rate, and discuss how you can leverage current trends to your advantage. If you want to make well-informed decisions, this article is your go-to resource.

Table of Contents

- What Is the Average Mortgage Rate?

- How Are Mortgage Rates Calculated?

- Factors That Affect the Average Mortgage Rate

- Why Do Average Mortgage Rates Fluctuate?

- How to Find Today’s Average Mortgage Rate?

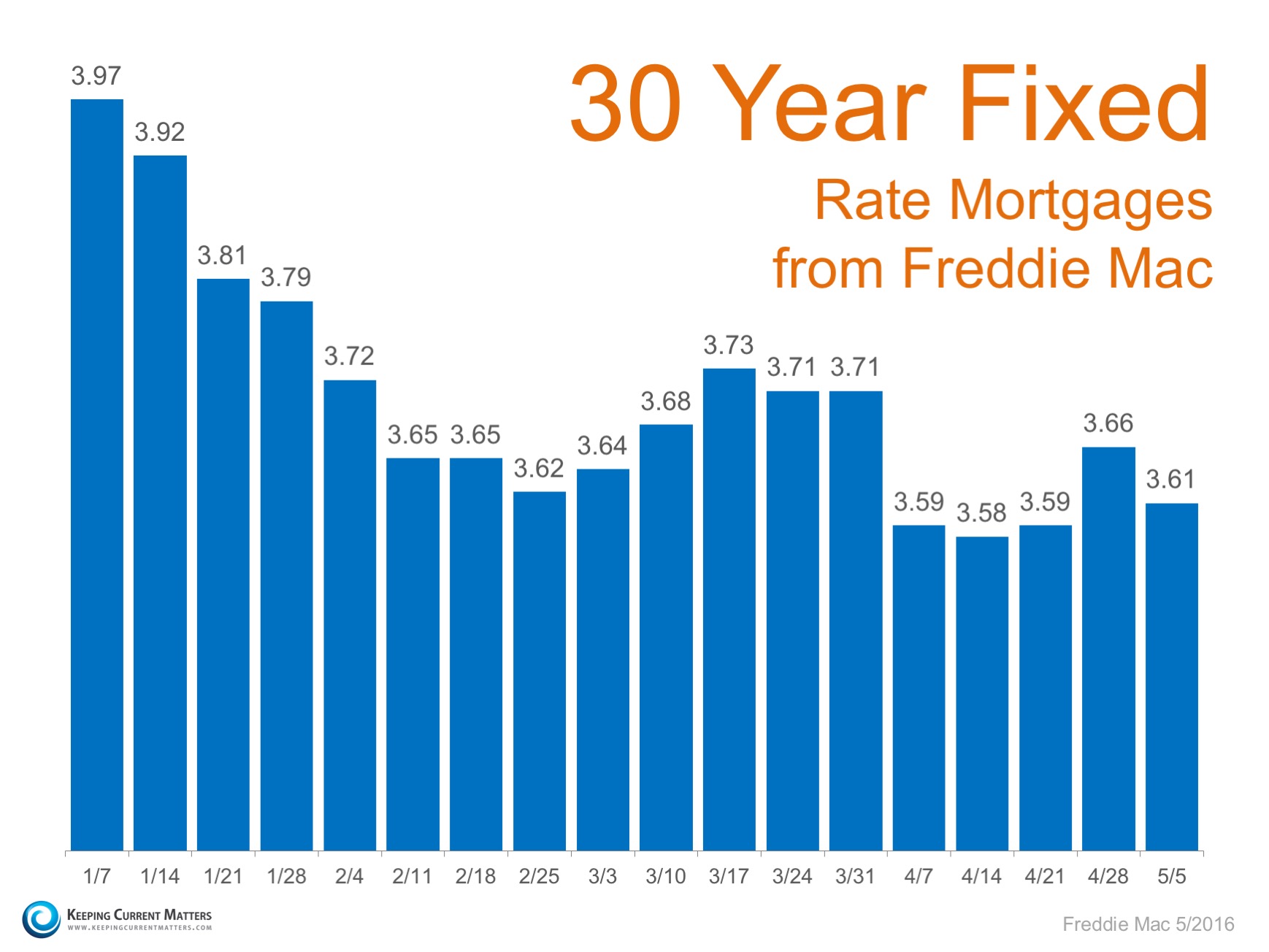

- Average Mortgage Rate Trends: What You Need to Know

- How Does the Average Mortgage Rate Impact Homebuyers?

- Average Mortgage Rate for Fixed vs. Variable Loans

- Tips for Locking in the Best Mortgage Rate

- Is It a Good Time to Buy a Home?

- How Long Should You Monitor the Average Mortgage Rate?

- Regions with the Lowest Average Mortgage Rate

- How the Federal Reserve Influences Mortgage Rates

- Common Mistakes to Avoid When Checking Mortgage Rates

- Future Predictions for the Average Mortgage Rate

What Is the Average Mortgage Rate?

The average mortgage rate is the mean interest rate that lenders charge borrowers for home loans. This rate is typically expressed as a percentage and reflects the cost of borrowing money to purchase or refinance a home. It’s calculated based on data from various lenders and encompasses different types of loans, including fixed-rate and adjustable-rate mortgages.

How Are Mortgage Rates Calculated?

Mortgage rates are calculated based on a variety of factors, including the borrower’s credit score, loan amount, loan term, and the overall risk associated with the loan. Lenders also consider broader economic factors, such as the federal funds rate, inflation, and bond market trends, when determining mortgage rates.

Factors That Affect the Average Mortgage Rate

Several factors influence the average mortgage rate, including:

- Economic conditions, such as inflation and unemployment rates

- Monetary policies set by the Federal Reserve

- Demand and supply in the housing market

- Borrower-specific factors like credit score and debt-to-income ratio

Why Do Average Mortgage Rates Fluctuate?

Mortgage rates fluctuate due to changes in economic conditions, market demand, and government policies. For example, if inflation rises, lenders may increase rates to maintain profitability. Similarly, changes in the Federal Reserve’s monetary policies can lead to rate adjustments.

How to Find Today’s Average Mortgage Rate?

Finding today’s average mortgage rate is easier than ever. You can check online resources, consult financial news outlets, or speak with mortgage lenders directly. Websites like Freddie Mac and the Mortgage Bankers Association also publish weekly updates on average rates.

Average Mortgage Rate Trends: What You Need to Know

Tracking trends in the average mortgage rate can help you predict future changes and make informed decisions. For instance, if rates have been steadily declining, it might be a good time to lock in a rate for your mortgage. Conversely, rising rates may indicate a need to act quickly to secure favorable terms.

How Does the Average Mortgage Rate Impact Homebuyers?

The average mortgage rate significantly impacts homebuyers by affecting the affordability of monthly payments. A lower rate means you’ll pay less in interest over the life of the loan, whereas a higher rate increases your overall borrowing costs.

Average Mortgage Rate for Fixed vs. Variable Loans

The average mortgage rate varies between fixed-rate and variable-rate loans. While fixed-rate loans offer stability with consistent payments, variable-rate loans typically start with lower rates but may fluctuate over time based on market conditions.

Tips for Locking in the Best Mortgage Rate

To secure the best mortgage rate, consider the following tips:

- Improve your credit score by paying off debts and avoiding late payments.

- Shop around and compare offers from multiple lenders.

- Consider a shorter loan term to qualify for lower rates.

- Lock in your rate to protect against future increases.

Is It a Good Time to Buy a Home?

Determining whether it’s a good time to buy a home depends on various factors, including the current average mortgage rate, your financial situation, and market conditions. If rates are low and your finances are in order, it could be an opportune time to make a purchase.

How Long Should You Monitor the Average Mortgage Rate?

It’s advisable to monitor the average mortgage rate for at least a few months before making a decision. This allows you to identify trends and better understand when to lock in a favorable rate.

Regions with the Lowest Average Mortgage Rate

Regional variations can impact the average mortgage rate. States with lower housing demand or more competitive lending markets may offer better rates. Researching rates in different areas can help you find the most affordable options.

How the Federal Reserve Influences Mortgage Rates

The Federal Reserve indirectly influences mortgage rates through its monetary policies. By adjusting the federal funds rate, the Fed can make borrowing cheaper or more expensive, which in turn impacts mortgage rates.

Common Mistakes to Avoid When Checking Mortgage Rates

When researching mortgage rates, avoid these common mistakes:

- Failing to consider additional fees, such as closing costs

- Not comparing rates from multiple lenders

- Overlooking the impact of your credit score

- Ignoring rate trends and market conditions

Future Predictions for the Average Mortgage Rate

Experts predict that mortgage rates will continue to fluctuate in response to economic conditions. Staying informed about these projections can help you make strategic decisions about buying, refinancing, or investing in real estate.

You Might Also Like

The Ultimate Guide To Turtle Food: Nutrition, Types, And Feeding TipsUnderstanding Car Wrap Prices: A Comprehensive Guide

Madame Du Barry: The Scandalous And Alluring Mistress Of King Louis XV

The Ultimate Guide To Finding The Perfect Cilantro Substitute

The Legendary Tale Of King Midas: A Journey Through Myth And Morality

Article Recommendations

- One Direction Liam Payne Zayn Malik A Look Back

- Alex Lagina And Miriam Amirault Wedding

- Merylstreep_0.xml